After 2 years of high prices in the solar PV value chain, mostly for polysilicon, things are getting better as more capacity comes online bringing down its prices for the key raw material of solar wafers. However, it is now these wafer prices that might fuel a price war – as Bloomberg termed it – in the market after the world's largest PV manufacturer LONGi decided to slash prices by as much as 30% and that too soon after the world's largest solar show SNEC 2023 closed its doors.

On May 29, 2023, LONGi announced a 32% drop in its price for p-type M10 150μm mono wafer (182/247mm) to RMB 4.36 ($0.62) from RMB 6.3 ($0.89). Similarly, the price for p-type M6 150μm Mono Wafer(166/223mm) was lowered 30% from RMB 5.44 ($0.77) to RMB 3.81 ($0.54) (see China Solar PV News Snippets).

Primarily it seems to be a reaction of LONGi to its direct competitor, the other wafer big wig, TCL Zhonghuan, which brought down its wafer prices by more than 14% on May 11, 2023 to RMB 5.00 ($0.0640) for 182mm 150μm wafer, from RMB 5.84 ($0.748) announced on May 5, 2023. Now, LONGi's wafer prices are even lower than TCL.

While this seems to be the case, solar analysts believe the LONGi is striving to gain more market share with this price cut as it cushions itself with its economies of scale, market position and the general oversupply situation in the global markets. If this continues, it will make life very difficult for new wafer capacities, especially of smaller companies. As silicon prices have already decreased nearly 50% year-to-date, this has left some cushion for wafer companies.

It remains to be seen when the prices of M10 wafers go below RMB 4.0 ($0.56)/piece. It also needs to be seen if TCL or other wafer makers will strike back with another cut in wafer prices. The wafer price erosion comes as a record number of companies exhibited at SNEC, even showcasing their products in a car parking as the trade fair was fully sold out, and several hundred thousands of visitors attended.

Recently InfoLink Consulting pointed out the reason for this oversupply of wafers. According to its analysts, crystal pulling activity of mainstream companies has been lowered to varying degrees, and demand for production materials has shrunk significantly which has stimulated the price of silicon materials to 'decline in disguise'.

"However, for single in terms of the impact on the output of silicon wafers, the impact of the downward revision of wafer pulling will gradually be reflected in June, and it is difficult to have a short-term impact on the current phenomenon that the supply of monocrystalline silicon wafers exceeds the demand," opines InfoLink.

Developments in the PV industry just before, during and soon after SNEC point towards strongly growing demand for solar installations globally, but production capacities are growing even more. For instance, since Dec. 2022, Canadian Solar has upped its expansion plans by 3 times from wafers to modules (see Gigantic Expansion Plans From Canadian Solar). Another example is JinkoSolar, which has just announced RMB 56 billion investment to build a massive fab complex to host 56 GW annual capacity each for monocrystalline silicon pull rod, silicon wafer, high efficiency solar cells and modules (see Massive PV Manufacturing Complex In China). Only in its first quarter results published in early May, Jinko said that by the end of 2023, it targets to increase its annual production capacity for mono wafers and cells to 75 GW each and 90 GW for solar modules, up from 65 GW, 55 GW and 70 GW, respectively at the end of 2022 (see JinkoSolar Shipped 13 GW+ Solar Modules In Q1/2023). You can read about new expansion announcements for established players and newcomers day in day out in our daily Chinese PV Snippets (see yesterday edition here).

The interesting question now is how this trend is going to impact module prices and therefore their global demand this year, although this is not only a question of price.

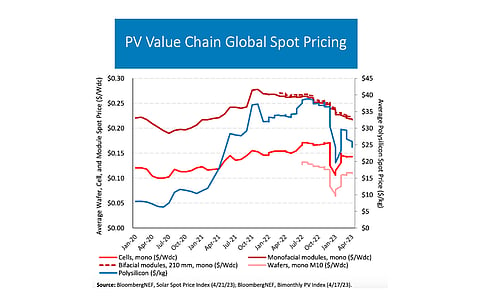

In its Spring 2023 Solar Industry Update, the National Renewable Energy Laboratory (NREL) charted the price fluctuations for various PV components and found and M10 mono wafer prices to have dropped significantly in January 2023, but went up in March, before they started to drop again in May. Module prices also had this steep drop in January, which recovered a little, before it continued its downward journey already in March. The brief drop beginning of the year was Covid-related; installations stalled, inventories piled up, prices dipped, mostly for silicon.

Prices for monofacial modules, however, have been dropping consistently since H2/2022, after the Covid-induced supply chain issues have been overcome. However, despite strong demand module prices were 'reaching lows in April 2023 that have not been seen for 2 years'.

Chinese modules are not as welcome in the US as earlier due to tariff issues and the Uyghur Forced Labor Prevention Act (UFLPA), while another big market with an appetite, India is also very protective, making it hard for Chinese modules to enter the market.

Europe with its need for energy security and carbon neutrality goals is a big buyer of Chinese modules. China was the largest solar module suppliers to Europe last year, shipping 86.6 GW to the continent in 2022, but Europe deployed only half of this quantity meaning there is still a lot of inventory left from last year for the region to use.

Still, in the first 2 months of the year, this pattern continued. While China shipped 17 GW modules to Europe, it supplied only a mere gigawatt to India and about 4.5 GW to the Americas (see Europe Imported 17 GW Chinese Modules In 2M/2023). But now distributors' warehouses in Europe are full, according to several sources. With the fear of blackouts or no gas for heating in the winter left behind for the moment, demand is not as big in Europe as a few months ago, let aside there's still a shortage of installers in many European markets, and permitting times pose a bottleneck for utlity-scale-scale PV power plants.

With the world's second largest solar show, Smarter E / Intersolar, taking place in Munich from Jun 14-17, only 3 weeks after SNEC Shanghai, and being sold out as well, it will be interesting to see the price points at which Chinese manufacturers will try to sell their products. Because one thing is clear. No matter if the global PV market will be 350 GW, as several solar market researchers believe, or even as large as around 400 GW, which is the estimate LONGi President Li told TaiyangNews in an exclusive interview, supply will be much larger. So product prices will fall further – for silicon, wafers, and modules.