Daqo New Energy produced 123,652 MT of polysilicon in 2025, meeting its guidance, while sales of 126,707 MT exceeded production

Utilization rates improved steadily from 33% in Q1 to 55% in Q4, even though revenue declined to $665 million from $1.0 billion in 2024

EBITDA for the year turned positive at $1.7 million compared to a negative $337.4 million in the previous year; net loss narrowed to $170.5 million

Management said polysilicon prices rebounded in H2 2025, supported by China’s anti-involution measures and industry self-discipline to curb excess capacity

For 2026, Daqo expects to produce 35,000 MT to 40,000 MT in Q1 and between 140,000 MT and 170,000 MT for the full year

Daqo New Energy Corp. increased output and reduced losses in 2025 as market conditions improved during H2. The Chinese polysilicon producer said rising utilization rates (from 33% in Q1 to 55% in Q4) and positive cash flow ($56.1 million, versus a $435 million outflow in 2024) helped offset weaker ASPs.

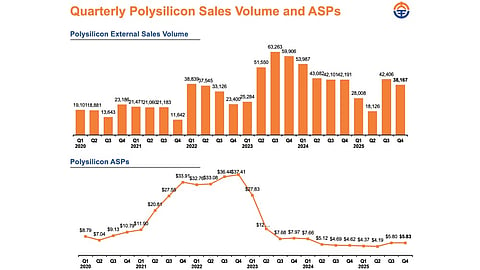

The company produced 123,652 metric tons (MT) of polysilicon last year, in line with its guidance of 121,000 MT to 124,000 MT. Its polysilicon sales for the period exceeded guidance, totaling 126,707 MT. The average selling price (ASP) decreased 7.2% YoY to $5.25/kg, from $5.66/kg in 2024.

Revenues of $665 million in 2025 were down from $1.0 billion a year earlier, driven by lower prices and reduced volumes (see Daqo New Energy’s FY2024 Revenues Declined By 56% YoY).

Despite the revenue decline, Daqo turned EBITDA positive at $1.7 million, compared to a negative $337.4 million in 2024, while net loss narrowed to $170.5 million from $345.2 million.

Sales volume in Q4 reached 38,167 MT, while production was near the high-end of the guidance range at 42,181 MT. The company stated that it focused on reducing production costs through process improvements, manufacturing efficiency gains, and raw material cost optimization during the period. Production costs declined 9% sequentially from $6.38/kg in Q3 2025 to $5.83/kg in Q4 2025.

Nevertheless, there was an ASP improvement in H2 compared to H1, which Daqo CEO Xiang Xu attributed to China’s anti-involution measures, as these supported the solar PV industry’s gradual recovery from a cyclical downturn, with polysilicon prices showing the strongest rebound.

“Looking ahead, we expect anti-involution initiatives will remain a central theme for the solar PV industry, supporting a more balanced supply and demand dynamic and driving higher-quality growth through 2026,” added Xu.

Xu also referred to major polysilicon manufacturers’ enforcing self-discipline to combat excess capacity and lower pricing (see Chinese Polysilicon Makers Join Hands Amid Overcapacity Concerns). He shared that these efforts reduced production volumes by 28.4% YoY to 1.32 million MT in 2025, leading to market prices going up by more than 50% from the mid-2025 lows to RMB 50 to RMB 56/kg by year-end.

In Q1 2026, Daqo targets to produce 35,000 MT to 40,000 MT of polysilicon and approximately 140,000 MT to 170,000 MT during FY2026.