CareEdge projects India’s solar module manufacturing capacity to reach 250 GW by FY2030

India’s solar module exports could rise to around 33 GW by the end of this decade as domestic capacity expands

Backward integration into cells, wafers, and ingots is expected to reduce India’s import dependence and strengthen supply-chain resilience

India’s solar manufacturing sector is expected to expand significantly over the next 5 years, with domestic solar module manufacturing capacity projected to reach around 250 GW by FY2030, according to a report by CareEdge Analytics & Advisory.

Supported by this growth in module manufacturing, India’s power capacity grew rapidly to 150 GW in FY26, accounting for 28% of the country’s total installed power capacity, up from 9% in FY20. India’s solar PV capacity additions are expected to nearly double to about 290 GW by FY30, supported by annual additions of around 35 GW, according to CareEdge.

However, the projection seems conservative, as in FY2026 India’s total installed solar PV capacity was pegged at 44.6 GW in AC terms, and the market is likely to grow by around 50 GW according to projections from JMK Research (see India Adds Record 45 GW Solar PV Capacity In FY 2026).

Backed by supportive government measures, including the Approved List of Models and Manufacturers (ALMM), Production-Linked Incentive (PLI) scheme, Basic Customs Duty (BCD), and GST rationalization, India is increasingly focusing on backward integration across the solar value chain.

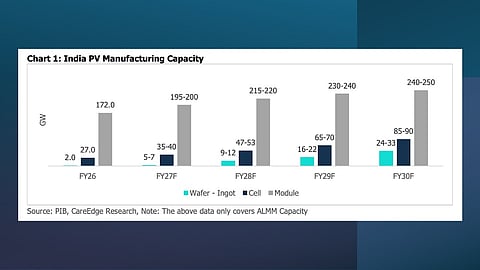

According to CareEdge, India’s solar module manufacturing capacity rose sharply from 13.6 GW in FY20 to 172 GW in FY26, while cell manufacturing capacity remains comparatively low, leaving the country reliant on imported cells and upstream materials such as wafers, ingots, and polysilicon. While CareEdge pegs India’s cell production capacity at 27 GW (up from 4.3 GW in FY20), India has over 30 GW of domestic production capacity enlisted in the Approved List of Models and Manufacturers (ALMM) List-II (see India Brings ALMM List-II For Solar Cells Into Force).

In FY25, Adani Group commissioned India’s maiden ingot and wafer production facility with 2 GW installed capacity. CareEdge projects India to expand its wafer-ingot manufacturing capacity to 5 GW to 7 GW in FY27, eventually reaching 24 GW to 33 GW in FY30. Cell capacity will expand to around 90 GW by the end of this decade.

According to CareEdge, building integrated manufacturing capacity across modules, cells, and ingot-wafer production could require cumulative investments of more than INR 80,000 crore by FY30.

Most of the ingot-wafer production capacity is planned by companies such as Adani Solar, Waaree Energies, Tata Power Solar, and Premier Energies, with around 10 GW capacity each.

“The country is also at the cusp of commencing domestic polysilicon production, with major fully integrated manufacturing facilities expected to come online between FY26 and FY28,” it stated.

This expansion is expected to reduce dependence on imports, particularly from China, while creating opportunities for exports. Analysts believe India’s solar module exports will exceed 30 GW by FY30.

While China continues to dominate the global solar manufacturing value chain, benefiting from large-scale integrated operations and lower production costs, analysts stress that India’s growing focus on backward integration, supported by policy incentives and private-sector investment, suggests a gradual shift from module assembly towards a more self-reliant and export-oriented solar manufacturing industry.

Speaking at the TaiyangNews Solar Technology Conference.India 2026 (STC.I 2026) earlier this year, EUPD Research Senior Consultant Rajan Kalsotra said India’s announced module capacity could rise to 190 GW by 2027 and 280 GW by 2030 (see India’s Solar Manufacturing Push Faces New Challenges Beyond Capacity Expansion).