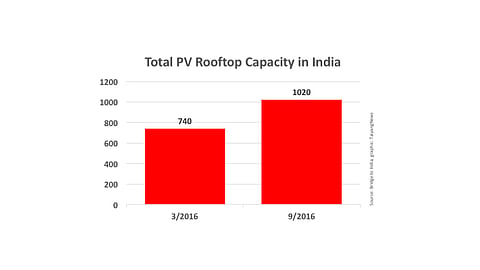

The cumulative rooftop PV capacity in India has crossed the 1 GW mark, after 513 MW were added in the last 12 months time. According to a blog post from clean energy consultancy Bridge to India on October 17, 2016, India's rooftop PV capacity now stands at 1,020 MW. At least 22% of the capacity additions last year was financed based on the so-called OPEX model, in other words third party owned solar systems.

The Government of India has an ambitious plan to have 40 GW of solar power capacity through rooftop by 2022. However, this segment is still in its infancy in the country while the government supports it with full vigor. Things seem to be changing for the better now as Bridge to India believes the country registered 300% growth for PV on rooftops over the last year (see Good Prospects For Rooftop Solar In India). International financial institutions, such as the Asian Development Bank and the World Bank, have pledged their resources to help India improve its rooftop PV capacity (see ADB Supports Indian Rooftop PV and World Bank Sings Loan Agreement With India).

Among the various stumbling blocks for rooftop PV in India is solar's upfront cost, which in particular private households or small enterprises have difficulties to stem. ha The private sector has thus been promoting a rooftop PV concept based on the so-called OPEX model. Herein, the developer owns the solar panel system, installs and finances it and sells the solar power generated to the rooftop owner under a long-term agreement. That means the developer basically takes over the role of a utility. The building owners need not purchase the PV system, and they get a 20% to 30% discount on grid power cost.

A number of Indian companies, including Cleantech Solar, Amplus Solar, Hero Future Energies, Azure Power, are also eyeing triple digit growth rates in this segment.

However, Bridge to India believes that for the OPEX model to work for developers to get the required return from rooftop projects, consumers need to consume all solar power generated and pay according to the long term agreement. With solar power's costs and prices quickly coming down, consumers of older projects may tend to default on their commitment. At the same time, there is the problem of banks accepting credit risk over the contract time of 15 to 25 years. Another issue is that the legal system in India is not really prepared to resolve such disputes in an appropriate time frame.

Bridge to India doesn't see any alternative to the OPEX model for PV rooftops in India. "In our view, growth of OPEX business model is absolutely essential for exploiting India's rooftop solar potential and getting close to the government's 2022 target of 40 GW. The policy makers need to find an urgent solution to this issue." And that solutions could be what some earlier studies have already suggested – setting up dedicated commercial courts, getting power distribution companies to intermediate and/or setting up a credit insurance mechanism, to help this segment grow.