JMK Research expects India to expand its annual solar installations in CY2026 by 42.5 GW

Solar makes up 78 GW (68 GW pipeline and 10 GW bidding) of India’s combined pipeline of solar, wind, hybrid, and storage projects at 169 GW

23 companies shipped about 14 GW of solar modules during Q4 2025, of which the top 5 players alone accounted for a 52% share

Tender activity slowed; RE+storage is becoming a preferred configuration for tenders

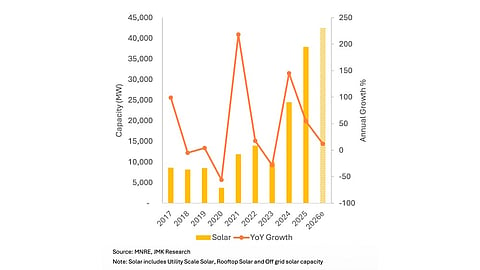

The Indian solar PV market is expected to install approximately 42.5 GW of new capacity in CY2026, which will be another annual deployment record after around 38 GW recorded for CY2025, a 54.7% annual increase, according to JMK Research & Analytics (see India Installed Close To 38 GW Solar PV Capacity In 2025).

About 16 GW is likely to come online over the next 2 quarters, according to analysts. New additions this year should include 32.5 GW of utility-scale, 8.5 GW of rooftop solar, and 1.5 GW from off-grid PV, compared to 28.6 GW, 7.9 GW, and 1.35 GW in the previous year (see India Installed Close To 38 GW Solar PV Capacity In 2025).

Thanks to solar, India recorded its largest-ever annual renewable energy additions last year. In its new quarterly report, JMK says most of the installation activity was concentrated in the states of Gujarat, Rajasthan, Maharashtra, Karnataka, and Tamil Nadu. Together, these states accounted for close to 84% of total solar and wind capacity additions last year, mostly solar. Gujarat alone commissioned 11.1 GW of capacity.

Solar continues to expand its share in the country’s total installed renewable energy capacity, which reached 258 GW as of December 31, 2025, as it accounts for 53% or 136 GW of the total renewables mix. Wind follows next with 21%, or 55 GW, and large-hydro 20%, or 51 GW.

India’s combined pipeline of solar, wind, hybrid, and storage projects currently stands at around 169 GW, comprising 68 GW of solar in the pipeline and 10 GW under bidding.

Manufacturing

At the end of 2025, India’s module manufacturing capacity reached 200 GW, of which 145 GW is part of the Approved List of Models and Manufacturers (ALMM) List-I, and the remaining outside of the list. JMK also counts India’s cumulative cell manufacturing capacity to have reached 31.17 GW as of 2025, of which 17.88 GW is enlisted under the ALMM List-II, also referred to as ALCM.

India’s upstream capacity continues to be limited with no domestic polysilicon production and only 8 GW to 12 GW of wafer-ingot manufacturing capacity, according to the JMK report.

During the reporting quarter, Insolation Energy added 4.5 GW and RPSG Solvanta 4 GW of module manufacturing capacity, while Waaree added 3.6 GW. Waaree’s total domestic module manufacturing capacity increased to 19.7 GW.

Among cell manufacturers, Jupiter International commissioned 1 GW and RenewSys 0.13 GW capacity.

Leading Suppliers

Among the leading solar module suppliers in Q4 2025, 23 companies together shipped about 14 GW, of which the top 5 players alone accounted for a 52% share. Waaree led the pack with a share of 21%.

Module exports were low, owing to the US tariff hikes bringing down their shipments to the American market, with the top 5 players exported only a little over 384 MW modules in Q4. While Waaree led the tally with 267.34 MW, it suffered a 65% drop from 758 MW in Q3 2025. However, Adani scored as its exports improved slightly to 111.2 MW, up from 100 MW in the previous quarter.

Among inverter companies, the top 3 suppliers were Sungrow, Sineng, and FIMER, which together accounted for around 73.9% of total inverter shipments. The top 15 companies shipped over 14.2 GW of central and string inverters during the last quarter of 2025. While Sungrow, Sineng, and FIMER shipped nearly 96.7% of all central inverter shipments, Sungrow, Sineng, and Polycab together accounted for 61.4% of all shipments among string inverters.

Tender Activity

India’s tender activity slowed down during the October-December 2025 period, with only 4.2 GW issued across solar, wind, hybrid, and RE+storage segments. This was a quarterly decline of 33% and an annual decline of 55%. Nevertheless, JMK highlights the growing role of dispatchable renewable power as 52% of all tenders during the quarter comprised RE+storage projects, thanks mainly to declining battery costs that have improved their viability.

“The slowdown in tender issuance can be attributed to multiple factors. Large capacities issued in earlier quarters led to temporary pipeline saturation, prompting a more cautious approach throughout the year. As a significant share of previously issued tenders has not translated into actual offtake, the government has slowed fresh issuances. Consequently, the Ministry of New and Renewable Energy has directed REIAs to review unsigned LoAs and prioritise clearing the existing pipeline before floating new bids, resulting in reduced tender issuance until backlog and viability concerns are resolved,” according to JMK analysts.

Additionally, given the land, transmission, and policy-related constraints, RE+storage projects require longer planning cycles, which again slows down tender rollout. In terms of allocation, close to 4.6 GW of the total tendered capacity was allocated last quarter.