Public auctions and corporate PPAs together supported 92 GW of solar installations in the EU between 2022 and 2025, according to a SolarPower Europe report

These provide a stable framework for investment and energy procurement to support the bloc’s energy transition, which must be continued

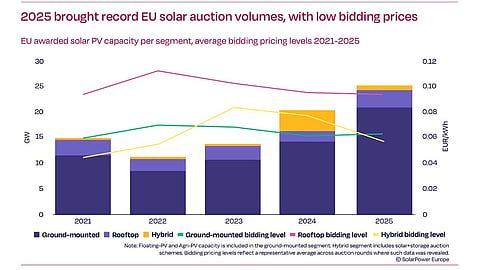

EU solar auction awards reached a record 25.2 GW in 2025, a 24% annual increase, with ground-mounted projects capturing over 80% of allocations

Corporate PPA volumes declined to 25.1 GW in 2025 after strong growth in 2023–2024, as price cannibalization, grid congestion, and curtailment slowed uptake

The association recommends improving auction design, supporting technology-specific tenders, integrating energy storage, and ensuring long-term policy visibility to sustain solar growth

Public energy auctions and corporate power purchase agreements (PPAs) drove 92 GW of solar installations in the European Union (EU) between 2022 and 2025, according to a new report by SolarPower Europe (SPE).

As EU policymakers seek effective ways to enhance energy price competitiveness, especially in the current geopolitical scenario, SPE recommends they continue with long-term PPAs and competitively awarded contracts for difference (CfD) as proven instruments at their disposal.

“As a new fossil energy crisis enfolds, and the EU solar roll-out is under pressure, SolarPower Europe’s latest report underlines that Europe must ensure healthy continuity for auctions and PPAs,” it explains.

According to the report, titled Auctions and Corporate PPAs: European Market Review 2025, these tools provided a stable investment framework and helped businesses and consumers manage energy costs in the aftermath of the 2022 energy crisis. In 2021, solar auctions peaked with 14.8 GW allocation, but dropped over the next 2 years, prompting individual countries to tweak auction designs to deal with higher equipment costs, low price caps, and slow administrative procedures, among others.

The comprehensive reforms paid off in 2025 when the EU awarded a collective 25.2 GW, a record representing a 24% annual increase. Ground-mounted solar rebounded strongly from an awarded capacity share of 70% in 2024 to over 80% of total allocations and exceeding 20 GW in 2025, helped by an increased share of rooftop and hybrid auctions. Competitive bidding, with prices about 20% below support ceilings, helped attract strong investor participation.

Germany was the largest contributor to the auctioned solar capacity, having awarded nearly 25 GW of solar PV capacity since 2021. Italy has started to leverage the auction route as a major deployment tool since 2024. According to the SPE report, Italy allocated 10.8 GW in 2025 under its FER X auction scheme, the highest awarded by a single EU country in a single year ever.

This success needs to be continued with more effective measures, including dealing with undersubscription, suggests SPE, calling it a ‘major missed opportunity for accelerating solar deployment’.

Calling auctions a ‘cornerstone’ of Europe’s strategy for scaling large-scale solar installations, analysts recommend a series of measures to improve their effectiveness. These include improving auction design, supporting technology-specific tenders, ensuring long-term investment visibility, and including storage in solar auction frameworks.

Corporate PPAs, on the other hand, boomed in the aftermath of the energy crisis in 2023 and 2024, but announced volumes in 2025 fell below a record 2024 to 25.1 GW. In the EU’s 2nd biggest market, Germany, volumes declined by 56%. SPE analysts list price cannibalization, grid congestion, and curtailment as playing spoilsport in the uptake of CPPAs.

Spain saw strong growth among the EU’s CPPA markets, with over 2 GW capacity signed up annually between 2023 and 2025, along with Italy, Poland, and Bulgaria – all heavily reliant on gas-fired generation. Corporations take the PPA route to cushion themselves against high wholesale electricity prices.

Analysts warn that these mechanisms are beginning to face new challenges, including market uncertainty and regulatory barriers in several countries. The industry group says maintaining strong and predictable auction and PPA frameworks will be critical to sustaining solar growth across the region.

“It’s now more crucial than ever that Europe boosts industrial electrification and access to PPAs, while also ensuring that auctions are well-designed to avoid missed opportunities and undersubscription. One clear short-cut? Making sure that storage is properly integrated across these two vital solar routes to market,” said SPE Deputy CEO Dries Acke.

The report writers offer 5-policy recommendations to maximize the positive impact of these tools. These include improving auction frameworks, supporting technologyspecific tenders, integrating energy storage, ensuring fair carbon accounting for PPAs, and accelerating electrification across the economy.

The report is available for free download on SPE’s website.