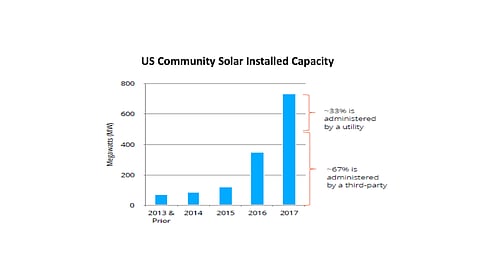

Cumulative capacity of US community solar at the end of 2017 reached 734 MW. This comes from a whopping 112% YoY growth of 387 MW in 2017, on top of the cumulative of 347 MW at the end of 2016, according to the Smart Electric Power Alliance's (SEPA) new Community Solar Program Design Models report.

This is huge compared to the total solar market in the country, which grew at an average annual rate of 68% over the last 10 years. Third party community solar providers are responsible for 495 MW or 67% of the total installed capacity. The other 239 MW is managed by utilities. It shows a shift that has come in since 2015 when the utility and third party split was 60:40.

A recently released GTM Research report, Commercial Solar Consumer Finance Trends, attributes intense growth in community solar to the growth of third party ownership (TPO) in the non-residential sector.

Dan Chwastyk, SEPA's program manager for community solar programs,sees a lot of potential in this segment, as it allowsutilities and third-party developers to customize offerings based on local markets and customer interests. "Our research and case studies show that the more tuned-in to their customers utilities are, the more innovative and successful their programs become," said Chwastyk.

Growth of community solar is likely to continue to be driven by falling solar costs, increasing consumer awareness of the business model and opening of new state markets thanks to regulatory push. SEPA points out that the factors that will determine the continued momentum in its growth will be states meeting their renewable portfolio standards as there is a greater mix of renewable energy generation in utility supply.

At present, 228 utilities in 36 US states have active community solar programs; the total number of utilities in the country stands at 3,100. This leaves out almost 90% of the US customers from opting for community solar. Third party administered capacity is concentrated in three states of Colorado, Minnesota and Massachusetts, as these states offer significant financial incentives.

Utilities are now exploring the use of community solar as a grid asset to improve reliability and grid support services. In a separate report titled Value Stacking in Minster, the authors share a case study of a community based solar power project that combines with a storage facility in the village of Minster, Ohio. This "partnership" allowed to generate four different value streams from a single project.

Getting the initial customers to sign up for the community solar program is the biggest challenge faced by utilities. For third-party administrators the major challenge is to meet complex and diverse policy requirements.

Both the reports are funded by the US Department of Energy's Solar Market Pathways Initiative.

A recent report from the US National Renewable Energy Laboratory (NREL) estimates 320 GW rooftop solar potential for low-to-moderate income households, which includes community solar (see 320 GW PV Potential From US Low-Income Households).