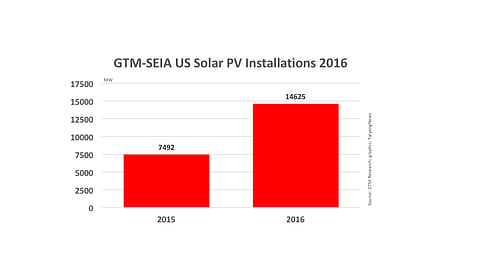

The US installed 14,625 MW of solar PV in 2016, increasing 95% over 7,493 MW installed in 2015. This is even higher than the 13.9 GW it forecasted for the full year in its Q3/2016 report. And what's even more impressive: Solar ranked as the number one source of new electric generating capacity additions on an annual basis, for the first time ever.

Solar accounted for 39% of all new capacity additions in 2016, across all fuel types, according to the upcoming 'US Solar Market Insight report', scheduled to be released on March 9, 2017. GTM and the US Solar Energy Industries Association (SEIA) previewed the data, which shows utility scale solar was the driving force behind the huge tally for 2016. It had the highest growth rate of any segment, growing 145% from 2015.

"Solar's economically-winning hand is generating strong growth across all market segments nationwide, leading to more than 260,000 Americans now employed in solar," said Abigail Ross Hopper, SEIA's newly appointed president and CEO (see New CEO For SEIA).

Most of the market growth took place in the utility-scale segment, which were installed from the pipeline of projects that were developed initially in preparation for the originally anticipated expiry of the Investment Tax Credit that was surprisingly extended. Cory Honeyman of GTM Research said, "While US solar grew across all segments, what stands out is the double digit gigawatt boom in utility-scale solar, primarily due to solar's cost competitiveness with natural gas alternatives."

The residential segment grew 19% from the previous year by a total of 2,583 MW. In the residential segment, 22 states added more than 100 MW each.

Community solar added more than 200 MW, with the maximum capacity coming up in Minnesota and Massachusetts. Along with community solar, the non-residential solar market was also led by rate design and net energy metering that led to growth in installations in major state markets, specially California.

On the whole, the US now holds a cumulative solar PV installed capacity of over 40 GW with more than 1.3 million installations.

The full Q4/2016 report can be bought from GTM Research on its website for $3,995.