A new Carnegie Endowment report says China accounts for around 98% of global LFP production capacity

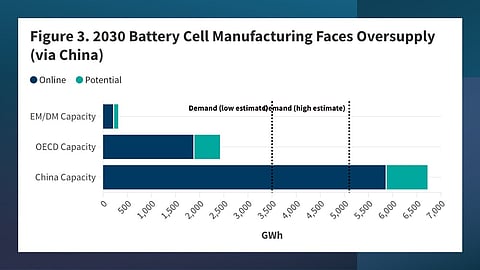

China's total battery cell capacity could reach at least 5,862 GWh by 2030, about 3 times the OECD's combined capacity

Carnegie warns that OECD economies could also fall behind China in emerging sodium-ion technology

China's dominance of lithium-iron-phosphate (LFP) batteries has emerged as the most pressing diversification challenge for OECD economies, according to a new Carnegie Endowment for International Peace analysis.

Currently, China accounts for around 98% of global LFP production capacity, while the chemistry now represents about half of the global lithium-ion battery market.

In its report titled Battery Geopolitics: Balancing Industrial Power in the Race to Store Energy, Carnegie said China's lead in LFP could be followed by a similar advantage in sodium-ion batteries. It called for coordinated action among major economies to retain competition in current and next-generation battery technologies.

The wider manufacturing gap is also set to increase. According to the analysis, China's battery cell production capacity could reach at least 5,862 GWh by 2030, around 3 times the combined 1,881 GWh projected for OECD countries. This data is based on projects under construction, it adds.

Chinese capacity has an ‘upper-bound’ potential of 6,720 GWh, which could exceed the estimated 5,100 GWh global battery cell demand. OECD factories, by comparison, will have a combined capacity of 1,881 GWh, with an upper-bound capacity of 2,422 GWh.

The US alone is expected to account for about half of OECD capacity, while Europe could have around 690 GWh. Analysts peg emerging and developing markets to account for only about 217 GWh, mainly split between India and Indonesia.

Carnegie said LFP is the most urgent battery diversification priority for OECD economies. The chemistry has lower costs than nickel-cobalt-based batteries and does not require expensive critical raw materials such as nickel and cobalt.

China's battery companies turned LFP from a relatively niche chemistry into a mainstream technology through lower costs and improvements in energy density, according to the report. The cost advantage remains difficult for overseas producers to match thanks to access to cheaper materials and manufacturing equipment, along with more efficient production for the Chinese.

European LFP cells cost between 24% and 50% more than Chinese cells imported into the EU, while the cost gap for nickel-manganese-cobalt (NMC) cells ranges from 10% to 27%.

“Cost-competitive Western batteries are critical to creating a more balanced playing field for global production,” stress the writers.

Closing the LFP cost gap, according to the report writers, could require at least a 30% tariff or a US-style $30/kWh production tax credit (PTC), or a combination of the 2 measures. While the US and Europe are scaling domestic LFP cell manufacturing at present, their midstream materials supply remains ‘severely underdeveloped’. It recommends partnering with South Korean or Japanese battery producers in diversifying LFP cells and materials.

While China has a stronghold over LFP, which it says is unlikely to be replaced in the medium or long term, Carnegie also warned that OECD countries risk falling behind China in the next promising alternative chemistry – sodium-ion technology.

China already leads in sodium-ion patents and first-of-a-kind commercial factories.

Sodium-ion is considered the next-generation battery chemistry most likely to become cost-competitive, though. Carnegie writers see it as complementing existing chemistries in stationary energy storage and short-range vehicles.

Nevertheless, analysts project China to have more than 500 GWh of sodium-ion battery factory capacity by 2030, exceeding the current lithium-ion capacity of either the US or Europe. China’s CATL alone plans to add 40 GWh of annual sodium-ion battery production capacity at its Fuding facility, and an additional 160 GWh at the Jining base in China (see CATL Debuts Commercial Sodium-Ion Energy Storage).

“The OECD partners are at risk of falling behind China on sodium-ion technology,” Carnegie said, calling for support to help the limited number of sodium-ion companies outside China reach commercial markets in the US and Europe.

Beyond sodium-ion, the report said OECD economies are comparatively well positioned in silicon-anode and lithium-metal technologies. It identified silicon-anode blends as a near-term opportunity to improve battery performance. This can help reduce graphite demand while using existing manufacturing infrastructure.

Carnegie calls for coordinated policy support and corporate partnerships between the US, Europe, South Korea and Japan.

“South Korea has the corporate prowess to produce and scale battery production, but it is at risk of falling further behind Chinese innovation in this domain. To buttress South Korea, the United States and Europe should prioritize opening their markets to South Korean conglomerates and focus diplomacy on battery innovation,” reads the report.