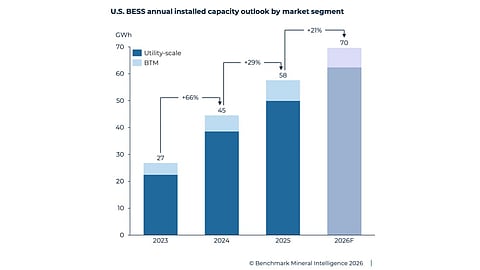

The US installed a record 28 GW/57 GWh of BESS in 2025, marking a 29% YoY increase, according to SEIA and Benchmark Mineral Intelligence report

Out of the total annual installations, nearly 30 GWh came from standalone storage projects, while around 20 GWh were paired with solar

Cumulative installed BESS capacity reached 137 GWh by the end of 2025, with 137 GWh utility-scale, 19 GWh C&I, and 9 GWh residential storage capacity

Residential deployments grew 51% to 3.1 GWh in 2025, ahead of the expiration of Section 25D tax credits, mainly driven by installations in California

The US had a record year of new battery energy storage system (BESS) installations in 2025 with a 29% year-on-year (YoY) growth. Out of 28 GW/57 GWh annual installations last year, standalone storage made up close to 30 GWh of new capacity, along with 20 GWh paired with solar, according to the U.S. Energy Storage Market Outlook Q1 2026 (ESMO) report.

The country’s cumulative installed BESS capacity at the end of 2025 reached 137 GWh.

Jointly launched by the Solar Energy Industries Association (SEIA) and Benchmark Mineral Intelligence, the report highlights strong growth in the US energy storage segment despite the federal government’s anti-clean-energy policies.

Interestingly, 2/3rd of all utility-scale energy storage capacity of 16 GW/50 GWh last year was installed in states that voted for President Donald Trump. Last year, there was a heavy concentration of utility-scale storage in the 3 markets of California (-21%), Texas (+67%), and Arizona (+129%). The pipeline of projects in this segment totals over 90 GWh, but analysts expect only 62 GWh of it to be realized as delays and cancellations mar the prospects of the others.

The behind-the-meter (BTM) market represented 12 GW/8 GWh of the total market.

Residential BESS deployments expanded by 51% annually to 3.1 GWh in 2025, led by California, mainly driven by the rush to install before Section 25D tax credits ended on December 31, 2025. For this reason, analysts peg residential BESS installations to decline by 49% in 2026 to 1.605 GWh.

According to the report, expansion of virtual power plants (VPPs) in states like Massachusetts, Texas, Arizona, and Illinois is driving residential storage deployment.

BTM deployments in the commercial and industrial (C&I) segment went up by 42% YoY to 2.61 GWh, driven mainly by 2 large Tesla Megapack installations at xAI’s Colossus Data Center. By 2030, the report projects data centers to account for 83% of BTM C&I installations in the US.

At the end of 2025, the US BESS market comprises 137 GWh of utility-scale, 19 GWh of C&I, and 9 GWh of residential storage capacity.

In 2026, the report writers expect annual BESS installations to increase to 35 GW/70 GWh, with the utility-scale market accounting for 20.2 GW/62.4 GWh, while BTM markets will contribute with 14.8 GW/7.3 GWh. By 2030, the report writers expect over 600 GWh of energy storage to be installed in the country.

The report covers various battery types. The US market is currently dominated by lithium-ion (majorly LFP). Its dominance is likely to persist, but its share may start to come down. In 2025, it accounted for 98% of all storage deployments in the country, but its share may drop to around 90% as sodium-ion, zinc-base, metal air, and flow batteries come into the picture by 2030.

Most battery cell manufacturers pivoted from EV manufacturing towards dedicated energy storage production as they converted existing lines. According to SEIA, the US had over 21 GWh of lithium-ion battery cell manufacturing capacity for stationary electricity storage applications, while the country’s capacity to manufacture BESS reached 69.4 GWh at the end of 2025.

“Whether it’s paired with solar or standing on its own, energy storage lowers consumer costs, makes the grid more reliable, and keeps the power on in homes during outages,” said SEIA Interim President and CEO Darren Van’t Hof. “Deployment is rising fast, but without a course correction from federal actions targeting the industry, Americans will face higher electricity prices and a less resilient energy system.”

The full report can be purchased on Benchmark’s website.

BloombergNEF says the global benchmark cost of a 4-hour battery project dropped 27% YoY to $78/MWh in 2025, a record low since 2009, thanks to lower pack prices, increased competition, and improved system designs (see Battery Storage Project Costs In 2025 Dropped To Record Lows Since 2009).