Governments in the US, Europe, and India are introducing incentives to build domestic solar manufacturing ecosystems

TOPCon is emerging as the preferred technology for many new solar factories, while HJT and back-contact remain alternative pathways

Higher construction, labor, and material costs continue to make solar manufacturing outside Asia more expensive than in China, says Peter Fath, CEO, RCT Solutions

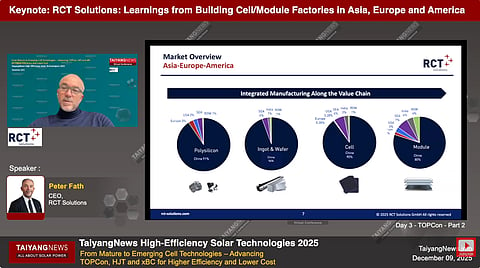

Solar manufacturing capacity has expanded over the past decade, but the global supply chain remains highly concentrated in Asia. China dominates most stages of PV manufacturing, from polysilicon to modules. As solar deployment accelerates worldwide, governments in the United States, Europe, and India are increasingly exploring policies to build domestic manufacturing ecosystems and reduce reliance on imports.

During the TaiyangNews High-Efficiency Solar Technologies Conference, Peter Fath, CEO of RCT Solutions, shared lessons from gigawatt-scale solar factory deployments worldwide. Drawing on the company’s experience supporting large PV manufacturing projects, he explains the economic, policy, and operational challenges of building cell and module factories outside Asia.

Building gigascale solar manufacturing facilities outside Asia involves more than installing production equipment. According to Fath, large-scale manufacturing requires trained personnel, a reliable supply of chemicals and consumables, strong logistics networks, and stable access to materials. To reduce exposure to dominant Asian solar manufacturing markets, major solar markets such as the United States, Europe, and India are introducing policy frameworks and incentive programs to promote domestic manufacturing.

In the United States, although it is on its way to being prematurely phased out, the Inflation Reduction Act (IRA) provides strong incentives for PV manufacturing. These include tax credits of $3/kg for polysilicon, $12/m² for wafers, $0.04/W for solar cells, and $0.07/W for modules. The policy also offers investment tax credits covering up to 30% of factory CapEx.

India has introduced similar incentives through its Production Linked Incentive (PLI) scheme. The program has awarded approximately 48 GW of module manufacturing capacity, supported by investments of over ₹93,000 crore. Türkiye also launched industrial initiatives, such as the HIT-30 program, which offers up to $2.5 billion in support for solar cell manufacturing projects with a minimum capacity of 5 GW.

In Europe, the Net-Zero Industry Act (NZIA) aims to ensure that 40% of the region’s demand for net-zero technologies is supplied by domestic manufacturing by 2030. Fath notes that despite policy support, establishing solar manufacturing in Europe remains difficult. The European solar market has stabilized at around 60 GW of annual installations, but the region’s manufacturing sector remains under pressure. Low-cost module imports from Asia have increased competition, putting several manufacturers in financial distress. According to Fath, NZIA could create new opportunities for domestic manufacturing if stronger local-content requirements are introduced.

Talking about the US, Fath says that the country has seen a surge in factory announcements since the IRA was introduced. According to Fath, more than $45.8 billion in solar manufacturing investments have been announced, potentially creating around 58,700 manufacturing jobs. Of this total, $9.1 billion is already operational, and $15.6 billion is currently under construction.

Another key decision for new solar factories is the choice of cell technology. According to Fath, many early manufacturing projects in the US initially planned to adopt heterojunction (HJT) technology. However, a large percentage of new facilities are now focusing on PERC or TOPCon production lines.

India’s emerging solar manufacturing sector is also largely centered on TOPCon cell factories, although some PERC lines are still being installed. In Europe, projects typically use TOPCon as the baseline technology, while allowing future upgrades to back-contact or tandem architectures. Fath emphasized that the most important requirement for new manufacturers is to produce a bankable product widely accepted in the market.

Industry forecasts suggest that TOPCon will remain the dominant solar cell technology through 2030 with more than 60% market share. HJT is expected to remain below 20%, while back-contact (BC) architectures could exceed 20%. Perovskite-silicon tandem technologies may reach around 1-2% market share if technical challenges are resolved.

Cost competitiveness remains one of the biggest barriers to solar manufacturing outside Asia. Fath presented a comparison of production costs across major regions. China continues to have the lowest costs due to its mature supply chain, large-scale manufacturing infrastructure, and lower equipment and construction expenses.

Factory construction in Europe and the US can be 2.1 to 2.6 times more expensive than in China. Labor costs in these regions are typically 3 to 4 times higher, while utilities such as electricity and water can be 20% to 60% more expensive. Material costs may also be 50% to 80% higher due to logistics and limited local supplier availability.

As a result, module production costs vary significantly by region. China can manufacture modules at approximately $0.11-$0.12/W. Costs in India may reach around $0.15/W, while Europe may range from $0.17 to $0.19/W depending on location. Manufacturing costs in the US are typically even higher.

Factory ramp-up also brings several operational challenges beyond cost considerations. Fath pointed to the importance of careful planning, contractor management, workforce training, and stable material logistics, noting that many manufacturers maintain several months of inventory for critical inputs to avoid supply disruptions during early production stages.

Fath also highlighted the growing interest in vertically integrated solar manufacturing projects outside Asia. Several companies are now planning facilities that integrate multiple stages of the PV value chain, from wafers and cells to modules, in order to strengthen domestic supply chains.

Fath concluded that solar manufacturing outside Asia requires careful planning and disciplined execution. Manufacturers must understand their target markets, technology choices, supply chains, and financing structures before launching large-scale projects.

He cautioned that rapid factory announcements without proper preparation can lead to overcapacity and financial risks. According to Fath, success ultimately depends on selecting the right project scope, building strong teams, and adopting a ‘zero-mistake’ approach during factory development and ramp-up.

To access the full presentation titled, Learning from Building Cell/Module Factories in Asia, Europe and America, click here.