- Markets

- Business

- People

- Opinion

- Technology

- Storage+

- Reports

- Our Events

- Tenders

- Price Index

- Top Modules

- ServicesServices

- AnalysisAnalysis

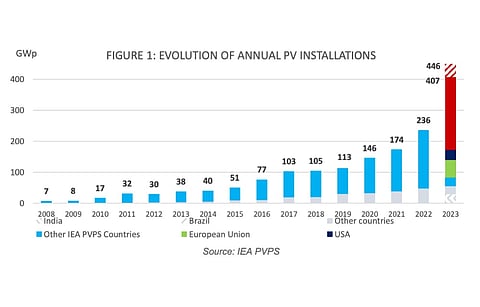

Solar PV module prices plummeted to record lows in 2023 due to a global oversupply situation, and electricity prices decreased after historical peaks in 2022, yet the technology managed to maintain its competitiveness. The world installed up to 446 GW DC of new PV capacity last year taking the global cumulative to 1.6 TW.

According to the Snapshot of Global PV Markets report of the International Energy Agency Photovoltaic Power Systems Programme (IEA PVPS) under task 1, the world now has a stock of 150 GW of solar modules. The consistent rise in module manufacturing capacity in 2023 largely 'outstripped' the market's ability to absorb new modules.

Additionally, transition of the industry from PERC to TOPCon is also majorly contributing to the inventory pile up. It has its repercussions. While China is not immune to the side effects of this inventory growth, the low prices and large inventories are particularly negatively impacting the slow development of local manufacturing projects outside of China and Southeast Asia.

Analysts point out, "This has comforted policymakers advocating for trade barriers and additional incentives for local manufacturing especially in the USA and India, and a vivid debate in the EU."

They add that massive increase in China's manufacturing capacity now makes it uncertain for local manufacturing projects in some individual markets, initiated in the previous years, to go ahead.

These difficulties in developing local PV manufacturing capacities in an already oversupplied market lead can also be leading to uneven political support for the industry.

Nonetheless, China continued to be the largest solar PV market, both in terms of the annual installed capacity of 235.5 GW DC, going up to 227 GW DC, as well as cumulative capacity of 662 GW DC. Its 2023 commissioned capacity accounted for more than 15% of the global total.

According to the IEA PVPS report, market growth outside of China reached an 'honorable' 30% while the Asian giant's own domestic growth was above 120%.

Europe brought online 61 GW DC, including 55.8 GW DC in European Union (EU). Germany led with 14.3 GW DC, followed by 7.7 GW DC in Spain, 6 GW DC in Poland, 5.3 GW DC in Italy and 4.2 GW DC in the Netherlands.

The US was next with 33.2 GW DC in the Americas, while Brazil installed 11.9 GW DC in the region.

India with 16 GW DC, was followed by 3.8 GW DC in Australia, 3.3 GW DC in Korea and 6.3 GW DC in Japan.

Overall, the number of countries with theoretical penetration rates over 10% doubled since last year to 18, and whilst smaller populations such as Spain, the Netherlands, Chile and Greece were leaders, more populous countries, including Germany and Japan also passed 10%.

The complete IEA PVPS report is available on its website for free download.