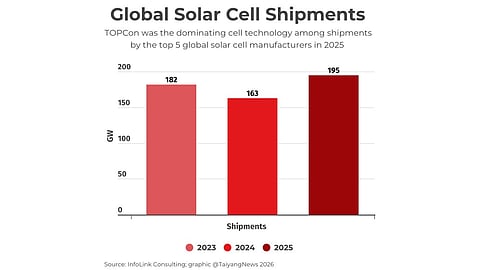

Global solar cell shipments by the world’s top 5 manufacturers rose about 19.8% YoY to 195 GW in 2025, according to InfoLink Consulting

Tongwei led the rankings, followed by SolarSpace and Yingfa Ruineng in second place, while Jietai Technology and Aiko Solar completed the top 5

TOPCon dominated technology share, while PERC accounted for around 10% and BC remained a small segment at about 1.7%

Solar cell prices were highly volatile in 2025 keeping manufacturers under pressure; they expect demand recovery this year

Global solar cell shipments by the world’s top five manufacturers—all Chinese—rose by about 19.8% year-on-year (YoY) to 195 GW in 2025, according to InfoLink Consulting with TOPCon making up 88.3% of total shipments. In 2024, the top 5 solar cell suppliers shipped a combined 163 GW (see Top 5 Solar Cell Suppliers Shipped 163 GW Capacity In 2024).

Tongwei continues to maintain its lead with the world’s “largest” silicon material and cell production capacity. It is followed by Zhongrun Solar Energy or SolarSpace and Yingfa Ruineng, both are tied for the 2nd spot on the list.

SolarSpace’s overseas shipment accounted for more than 30% of its annual total, according to InfoLink especially as its Laos located production base catered to India and America last year. This year things might change as shipments to the US from Laos will be subject to 80.67% countervailing duties (CVD) as per the preliminary determination by the US Department of Commerce. Final ruling is expected on July 6 this year (see India, Indonesia, Laos Solar Imports Face High US CVD Rates).

Yingfa Ruineng, currently the “only” professional manufacturer exporting back contact (BC) solar cells, thanks to its 6 GW cooperation with LONGi Green Energy Technology in 2024. The company maintained high production utilization in 2025.

One of the earliest TOPCon solar cell manufacturers, Jietai Technology or JTPV took 4th spot on the InfoLink list. Part of the Drinda Group, JTPC is building 10 GW n-type solar cell fab in Oman and is also pursuing a 5 GW cell fab in Turkey in collaboration with Schmid Pekintas Energy (see Drinda Announces 5 GW Solar Cell Factory In Turkey).

On the 5th spot is Aiko Solar which though proponent of BC technology currently has PERC cells dominating its shipments—60% of the total annual shipments.

PERC cells are expected to have accounted for 10% of the global cell shipments following 88.3% of TOPCon last year. BC cells still make up a minority of about 1.7%.

The market favored the 18X N (182–182.2 mm × 182–183.75 mm) cell format, with the top 5 manufacturers shipping a combined 77.8 GW last year—representing about 39.8% of total shipments. InfoLink expects them to have shipped a combined 56 GW of 210RN (182mm x 210mm) and 42 GW of 210N large sizes, accounting for 28.7% (2024: 19%), and 21.5% of total shipments respectively.

InfoLink analysts explain that by the end of 2025, both domestic solar manufacturers and customers had clearly started moving towards larger-sized solar cells. The 18X size is now mainly shipped to emerging markets such as India and Turkey, where the transition to new sizes is still in progress.

In 2026, InfoLink projects the 210RN size to keep gaining market share from 18X N and become the main shipment size across the global industry.

Analysts also touch upon the pricing environment of solar cells last year. For TOPCon the price rose above RMB 0.3/W thanks mainly to China’s 531 policy that became effective from June 1, 2025 (see World’s Biggest Solar Market Moving Towards CfD Mechanism).

In 2025, the solar cell market was highly volatile, with prices rising and falling sharply due to policy changes, raw material costs, and weak demand. Early policy support briefly lifted prices (to over RMB 0.3/W), but they soon dropped to near production cost (settling between RMB 0.23/W and RMB 0.24/W) as demand weakened.

Later in the year, rising silver prices pushed cell prices up again, even reaching high levels (RMB 0.38/W) at the end of December. However, end-user demand did not improve, and module manufacturers reduced purchases, leading to weak sales despite higher prices. As a result, solar cell companies continue to remain under strong operational pressure and are waiting for demand to recover this year, explains InfoLink.

Analyst opine, “In the future, only companies that can accurately respond to market challenges, continuously strengthen their brand competitiveness, and flexibly adapt to changes in the global political and economic environment will be able to solidify their position in a highly volatile environment and seize the next wave of growth opportunities.”

InfoLink’s 2025 solar module shipment tally counts nearly 536 GW shipped by 12 listed companies, with top 4 players—all Chinese—accounting for 58% of the total (see Top 4 Module Makers Control 58% Of 536 GW Global Shipments In 2025).