Daqo New Energy’s Q1 2026 revenue dropped sharply as shipments were scaled back amid weak prices and demand

Its net loss widened due to below-cost market conditions and lower sales volumes, according to the company

Management touts strong cash reserves and no debt as providing cushion, despite ongoing industry pressure

Daqo New Energy reported a sharp drop in revenue for Q1 2026, mainly due to lower sales volumes. The company scaled back shipments as polysilicon prices remained weak, resulting in a significant decline compared with both the previous quarter and the same period last year.

According to the Chinese solar-grade polysilicon manufacturer, Q1 2026 was affected by weak demand, high inventories, rising input costs, and geopolitical tensions, which pressured polysilicon prices and led to losses. Despite this, the company says it maintained strong liquidity with about $2.0 billion in cash and cash-equivalent assets and no debt, supporting its ability to manage the downturn.

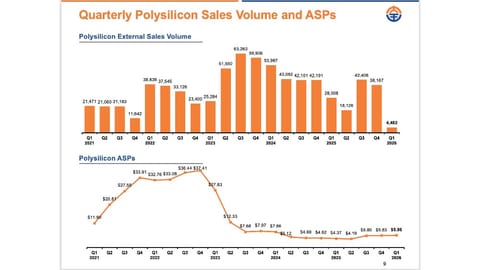

Its revenues for the reporting quarter at $26.7 million declined by 88% quarter-on-quarter (QoQ) and by over 78% year-on-year (YoY). Daqo sold 4,482 metric tons (MT) of polysilicon in Q1 2026, compared to 38,167 MT in Q4 2025 (see Daqo New Energy Swings To Positive EBITDA In 2025; Net Loss Declines).

Daqo’s net loss widened from $71.8 million in Q1 2025 and $7.3 million in Q4 2025 to $88.4 million for the Q1 2026.

The average selling price (ASP) for polysilicon during the quarter went up to $5.96/kg from $5.83/kg in Q4 2025. Daqo’s total production during the quarter totaled 43,402 MT, up from 42,181 MT in the previous quarter, at its 2 production facilities. With this, the manufacturer exceeded its guidance range of 35,000 MT to 40,000 MT.

Daqo New Energy CEO Xiang Xu shared, “With market prices for polysilicon experiencing a notable decline to be below production costs during the quarter ($5.95/kg), we adhered to the Chinese authorities' self-regulation guidelines by declining to engage in below-cost sales. We adopted a disciplined, wait-and-see approach pending further implementation of the national anti-involution policies we highlighted last quarter. As a result, our sales volume dropped to 4,482 MT, while our average selling price increased 2.3% sequentially to $5.96/kg.”

The company said it took proactive steps to manage weak market conditions, with capacity utilization at about 57%. Production and cash costs rose 2% and 3% QoQ, respectively, mainly due to exchange rates, but RMB manufacturing costs edged down despite higher silicon metal prices, supported by efficiency gains.

Industry utilization was around 39%, according to Daqo, amid low polysilicon demand and prices due to seasonality, weak demand, and ongoing overcapacity in Q1. Prices are now stabilizing, says Xu, while production cuts and expected government action address oversupply.

He specifically mentions a Chinese government meeting on April 17, 2026, wherein the authorities reportedly said that overcapacity is an urgent issue and want to control unfair market practices. All relevant authorities are required to deploy concerted measures across areas like controlling new capacity, setting standards, encouraging innovation, enforcing pricing rules, improving quality checks, supporting mergers and acquisitions, and protecting intellectual property.

Despite near-term pressure, the company remains optimistic about long-term solar growth, supported by energy security needs, and expects to benefit through its low-cost position, strong balance sheet, and focus on n-type technology and efficiency improvements.

“In light of the current market dynamics, we expect total polysilicon production volume in the second quarter of 2026 to be approximately 35,000 MT to 40,000 MT. For the full year of 2026, we expect production volume to remain in the range of 140,000 MT to 170,000 MT,” said Xu.