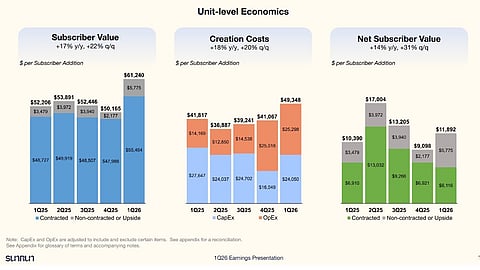

Aggregate creation costs for Sunrun fell 12% YoY to $872 million, though unit creation costs increased 18% due to larger systems and higher storage attachment rates

Sunrun says its aggregate subscriber value increased 13% YoY to $1.1 billion, with total subscribers crossing 1 million

The company added 17,665 new subscribers in Q1 2026, down 25% YoY, in line with its volume and margin optimization strategy

Sunrun has started fiscal year 2026 on a high note, with Q1 2026 revenue increasing 43% year-on-year (YoY) to $722.2 million, driven by customer agreements and incentives revenue, which improved 16% to $467.8 million. Nevertheless, its solar and storage installations during the quarter declined by 19% and 15%, totaling 154 MW and 282 MW, respectively.

Energy systems and product sales revenues of $254.4 million were up 151% YoY, with management attributing the increase to the sale of certain battery storage and energy systems linked to new customer contracts to another company.

While the aggregate creation costs of $872 million dropped by 12% over the same period, creation costs were 18% higher on a unit basis owing to higher system sizes, higher storage attachment rate, and adverse fixed cost absorption from lower volumes, explains the US-based home battery storage, solar, and home-to-grid power plants company.

Cash generation was negative $59 million and lower than guidance due to the company’s decision to shift certain project finance transaction activity from Q1 into Q2, according to CFO Danny Abjian. Analysts at ROTH note that this was the first quarter of negative cash generation for the company, having reported positive cash generation for 7 consecutive quarters, and management stressed that the delay is not related to a market slowdown.

During the reporting quarter, it added 17,665 new subscribers, representing a 25% YoY decline. Sunrun says this is in line with its volume- and margin-optimization strategy. It also reflects the decrease in lead-generation activities in mid-2025.

Sunrun added close to 19,000 customers in Q1 while its storage attachment rate rose to 73% for new customers. These customers can dispatch power to the grid when required. By the end of 2028, Sunrun expects to have over 10 GWh of dispatchable capacity online. At the end of the reporting quarter, it had networked storage capacity of 4.3 GWh with more than 251,000 solar and storage systems installed.

As of March 31, 2026, the company’s total subscriber count of 1,014,945 had increased 11% compared to a year earlier. Its aggregate subscriber value of $1.1 billion represented a 13% YoY increase.

Sunrun CEO Mary Powell said, “The proliferation of AI data centers, the electrification of transportation and homes, the decarbonization of the grid — all of these demand new solutions. The answer is not going to come from a single large plant that takes years and years to build. Instead, we believe distributed, intelligent, flexible resources deployed into homes and communities today will be a meaningful part of the solution.”

In 2025, Sunrun said it supplied nearly 18 GWh of electricity from home batteries to the grid across the US, with a peak output of 416 MW, comparable to the capacity of some fossil-fuel power plants. More than 106,000 customers joined its distributed power plant programs in 2025, up from around 20,000 in 2024. It claims these were used more than 1,300 times during the year to help reduce grid pressure, especially during periods of high electricity demand and extreme weather.

The company has reiterated its FY2026 forecast, expecting strong volume growth in its direct business, targeting cash generation of $250 million to $450 million. This excludes approximately $50 million to $100 million related to equipment safe harbor investments (see Sunrun Reports 45% Revenue Growth In FY2025 To $2.96 Billion).

Sunrun’s strategy is to continue allocating cash to reduce patent leverage and make final equipment safe harbor investments. It says the company will evaluate additional value-accretive capital allocation strategies depending on the market environment and outlook.