Key takeaways:

Residential solar in Europe is moving from PV-only systems to integrated setups with storage and energy management

Self-consumption, electricity cost savings, and backup power are the main drivers for this shift

Installers face challenges such as regulations, upfront costs, and labor shortages, while demand for integrated solutions continues to grow

The adoption of residential PV systems has been on the rise across Europe for some time now. As more and more Europeans opt for these systems, one key difference has emerged: a shift from PV-only to the integration of storage, energy management systems (EMS), etc.

At the TaiyangNews Smarter Solar for Homes & Businesses Conference, Ali Arfa from EUPD Research shared trends and key insights on the region’s rooftop solar market. He shared data from EUPD’s February 2026 prosumer and installer monitor surveys, before the Persian Gulf conflict.

In the context of the market, Arfa discussed the expectations of mature markets in the EU and the major shift in perspective from prosumers (producers + consumers) and installers. He stated that among the top 20 global PV markets per capita, 17 are European, with the Netherlands, Germany, Spain, and Austria taking the top 4 spots. And 20 of the 33 EU markets are rooftop-driven ones. These surveys, the Prosumer Monitor and the Installer Monitor, bring an EU perspective.

The Prosumer Monitor survey covers about 8,000 system owners in Germany and provides insights into technology adoption, brand perception, and investment trends. The Installer Monitor is based on an empirical survey of EU installers (~1,300), covering 13 major EU markets that account for more than 80% of all new PV installations in the EU.

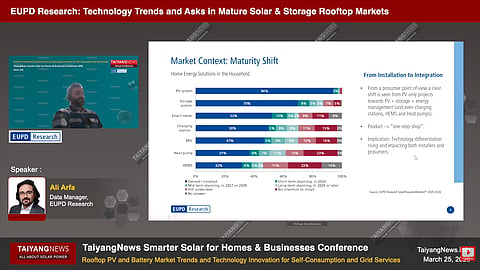

It was observed that from a prosumer perspective, there is a shift from PV-only projects to PV + storage + EMS (including charging stations, HEMS, and heat pumps). This impacts installers, as it was also observed that prosumers are looking for one-stop-shop solutions. For example, the Prosumer Monitor survey found that while 94% of prosumers have a PV system, 70% have storage installed, 50% have smart meters and charging stations, and about 30-35% have both HEMS and heat pumps installed. Therefore, there is a growing trend towards integrating distributed energy resources in residential settings. This shift is driven mainly by self-consumption, reduction in electricity costs, and emergency power supply, among others.

In terms of technology trends, Arfa highlighted that compact storage systems (≤5 kWh) are seeing increased adoption in rooftop installations and even more in non-rooftop PV, with about a 54% share in 2025. Plug-in PV systems see similar key drivers as overall installations, such as self-consumption and electricity cost savings. Additionally, easy installation and optimal use of space are key drivers for these types of systems. System integration is another important aspect that prosumers look for, rather than isolated technologies. The ability to integrate PV with storage, heating, EV charging, and EMS is becoming a key differentiator for installation companies, according to Arfa.

Barriers still exist, with economic viability and high upfront investment being the most important. Another key barrier is that about 30% of consumers expect storage prices to decrease in the coming years, which is leading to purchase postponement and, therefore, a delay in deployment.

From the perspective of installers, the key drivers are again self-consumption, rising EV demand, and EU directives and regulations. One interesting point was that 89% of German installers believe that growth in self-consumption and storage is a key driver for more PV installations, implying that PV is ‘piggybacking’ on storage rather than the other way around. Also, about 59% believe that the rise in demand for EVs is driving more PV installations, especially after the recent situation of war in the Strait of Hormuz.

German installers also see strong potential for residential and small commercial storage in the future. They believe there are growing opportunities for hybrid and smart inverters, smart meters, and bidirectional charging.

In conclusion to his talk, titled Technology Trends and Asks in Mature Solar & Storage Rooftop Market, Arfa also listed the existing barriers for installers, namely bureaucratic challenges in permitting and licensing, phase-out of feed-in tariffs, complex regulations, low electricity prices, labor shortages, etc.