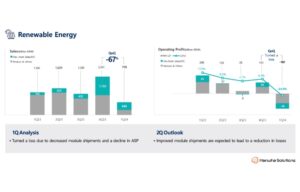

- SunPower says its Q2/2023 financials were marred by higher interest rates and higher cancellation rates in California

- Its residential customers totaled 20,400, up 3% on an annual basis from Q2/2022

- Company expects situation to improve in the near future as tax credit programs are implemented and retail utility rates increase while equipment prices come down

- SunPower Financial has signed on to become the exclusive lease and PPA provider for ADT Solar’s customers

US residential solar power company SunPower Corporation exited Q2/2023 with a GAAP net loss of -$30 million thanks to higher interest rates, even as its annual revenues improved 11%. Management anticipates better times ahead hoping for a decline in equipment prices, implementation of tax credit programs and increase in retail utility rates following heat waves.

The reporting quarter saw the company add 20,400 new residential customers, 3% higher than 19,700 it added a year ago, but a drop of over 2% from 20,900 it added in the previous quarter (see SunPower’s -$51 Million Net Loss In Q1/2023).

It blames lower demand, driven by higher interest rates and higher cancellation rates in California following NEM 3.0 wherein the state slashed its net metering rates for new customers from April 15, 2023 for the ‘softer’ market for residential solar.

New Homes business had $108 million in bookings in the quarter, reflecting an annual growth of 11% due mainly to sales outside California. It counts to have completed over 100,000 new home installations and has overall retrofit backlog of 20,000 customers and another 39,000 in the new homes department.

Management says the new homes backlog will benefit from customer recognition in 2024.

The management reiterated its lowered guidance for FY 2023, shared a week back wherein it expects to report GAAP net loss of -$90 million to -$70 million, and adjusted EBITDA of $55 million to $75 million. Previously it guided for adjusted EBITDA ranging within $125 million to $155 million (see SunPower’s Business Suffers With Dip In Demand).

While new bookings in California are on the decline for the company, Q2 bookings have been weaker than expected outside the state.

On a call with analysts to discuss Q2 results, CEO Peter Faricy said, “Long term, we continue to see substantial tailwinds for the US distributed solar market, including low market penetration, climbing utility bills, a strained electric grid, and a decade of tax benefits under the Inflation Reduction Act.”

SunPower also announced its in-house financial services division SunPower Financial signing agreement with ADT Solar becoming the exclusive lease and power purchase agreement (PPA) provider for the latter’s customers. The deal will enable ADT to provide flexible, accessible financing options to its rooftop solar and battery back-up customers.

This ADT Solar agreement helps it expand to new sources of customers beyond SunPower in 2024 and beyond. Philip Shen of Roth MKM sees this as a positive effort on part of the company to win new business with potential to drive a substantial amount of volume.